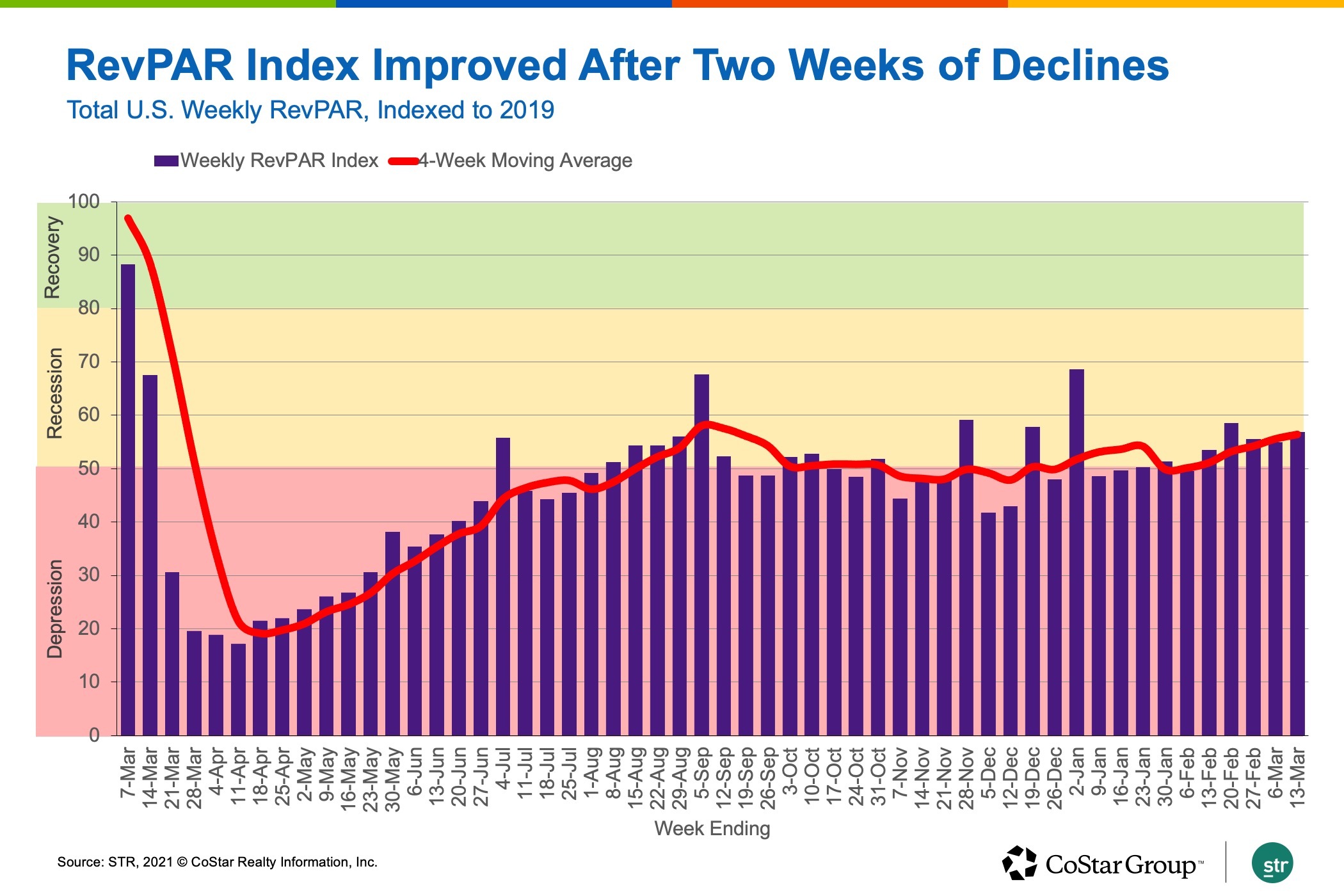

Weekly U.S. hotel revenue per available room, a key performance metric, achieved its highest absolute level and its lowest year-over-year decline since the COVID-19 pandemic began to take hold in the U.S. in mid-March 2020.

For the week ending March 13, U.S. hotel industry RevPAR was $53.45 — a decline of only 15.8% from the same week in 2020, which is mostly a function of easier comparisons, according to data from STR, CoStar’s hospitality analytics firm.

Follow Pigeon Forge News on Google News

However, STR’s Market Recovery Monitor, which compares current RevPAR performance against benchmark performance — the comparable week in 2019, considered pre-pandemic “normal” — shows that the U.S. hotel industry is still in the “recession” stage.

The Market Recovery Monitor places the industry and its markets into one of four categories, based on ratios achieved by dividing current RevPAR performance against performance in the comparable week in 2019. Ratios of 100 or more outperformed the benchmark, and below 100 underperformed. The categories are:

- Depression: Markets with an index of 50 or below against the benchmark;

- Recession: Markets with an index of between 50 and 79.9;

- Recovery: Markets with an index of between 80 and 99.9; and

- Peak: Markets with an index of 100 or higher.

The U.S. hotel industry RevPAR ratio for the week of March 13, 2020, is 57% of the level achieved in the comparable week in 2019.

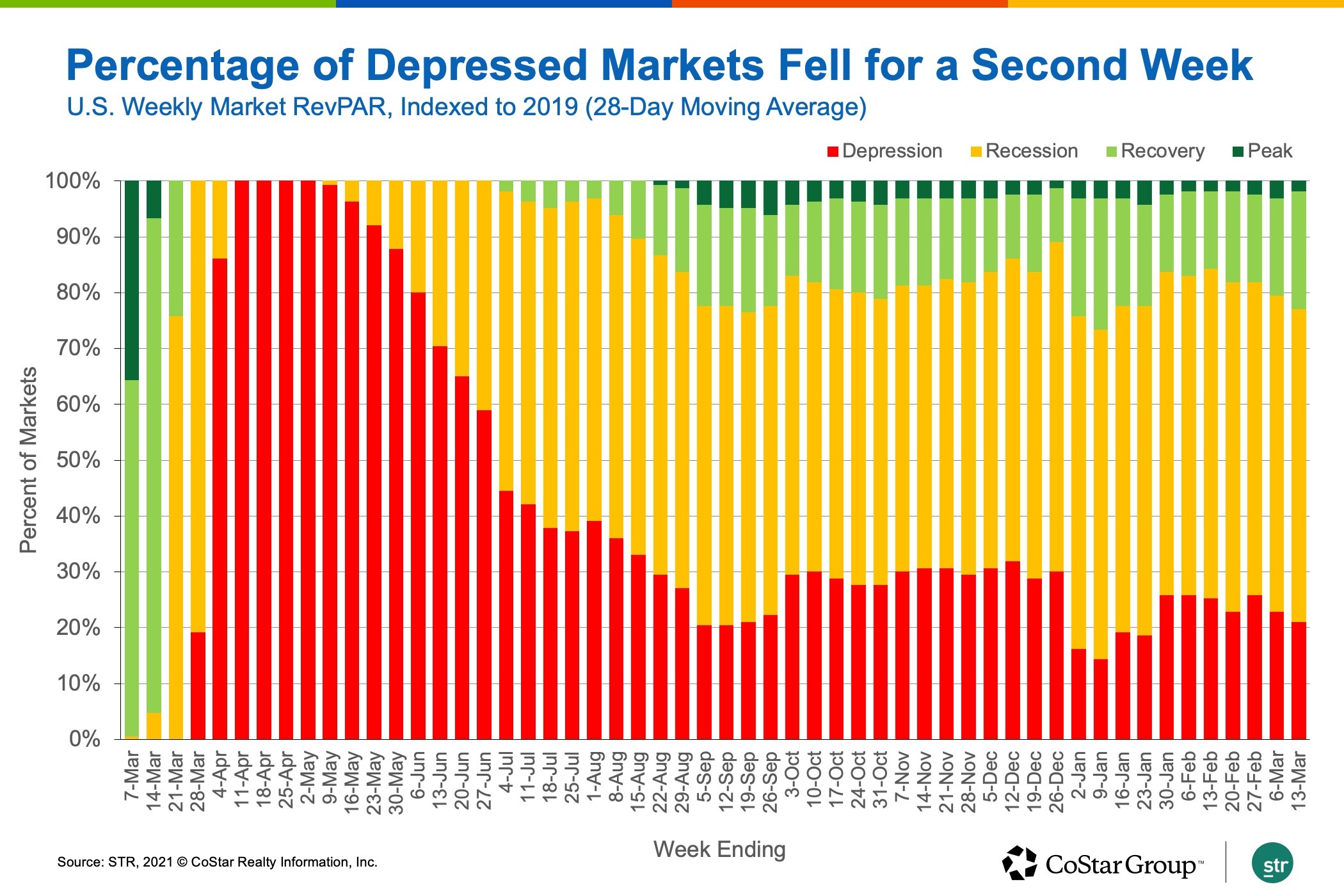

On a market level, the percentage of markets in the recovery category increased slightly for the week, and the percentage in the depression category decreased.

Of the 166 U.S. hotel markets in the STR database, 101 posted gains in 28-day RevPAR indexed to 2019.

The lowest indexed performance was recorded in San Francisco, and the highest indexed performance was in the Florida Keys, according to the recovery monitor.

By property type, larger urban hotels continued to be the most likely to post depression-level performance, while small hotels in smaller markets showed a higher likelihood of reaching RevPAR above 2019 levels.

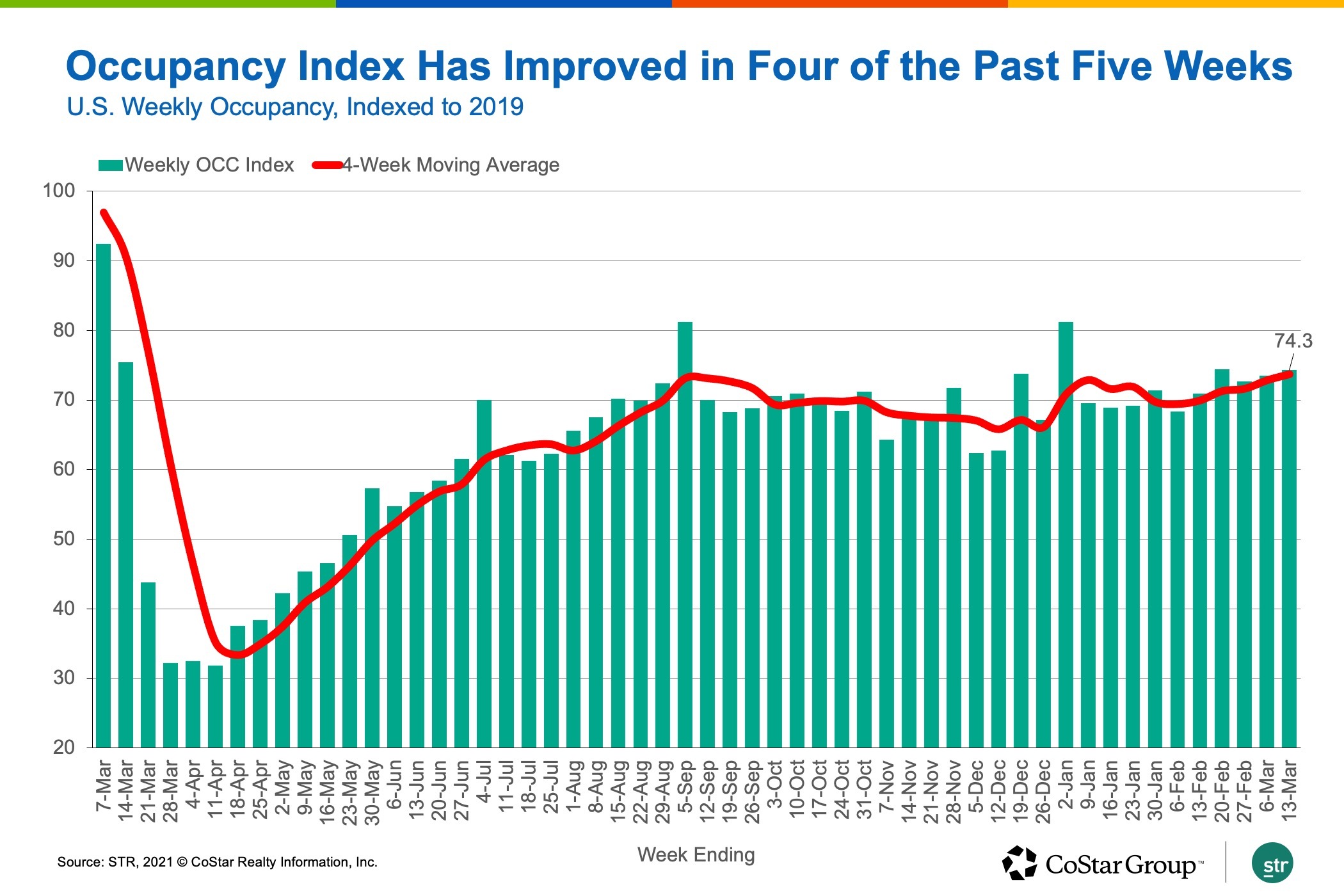

More than 19.3 million hotel rooms were sold in the week — the most of the past 52 weeks as demand rose by 1.2 million week over week. Hotel markets in all but seven states posted an increase in room demand, led by Florida and Texas.

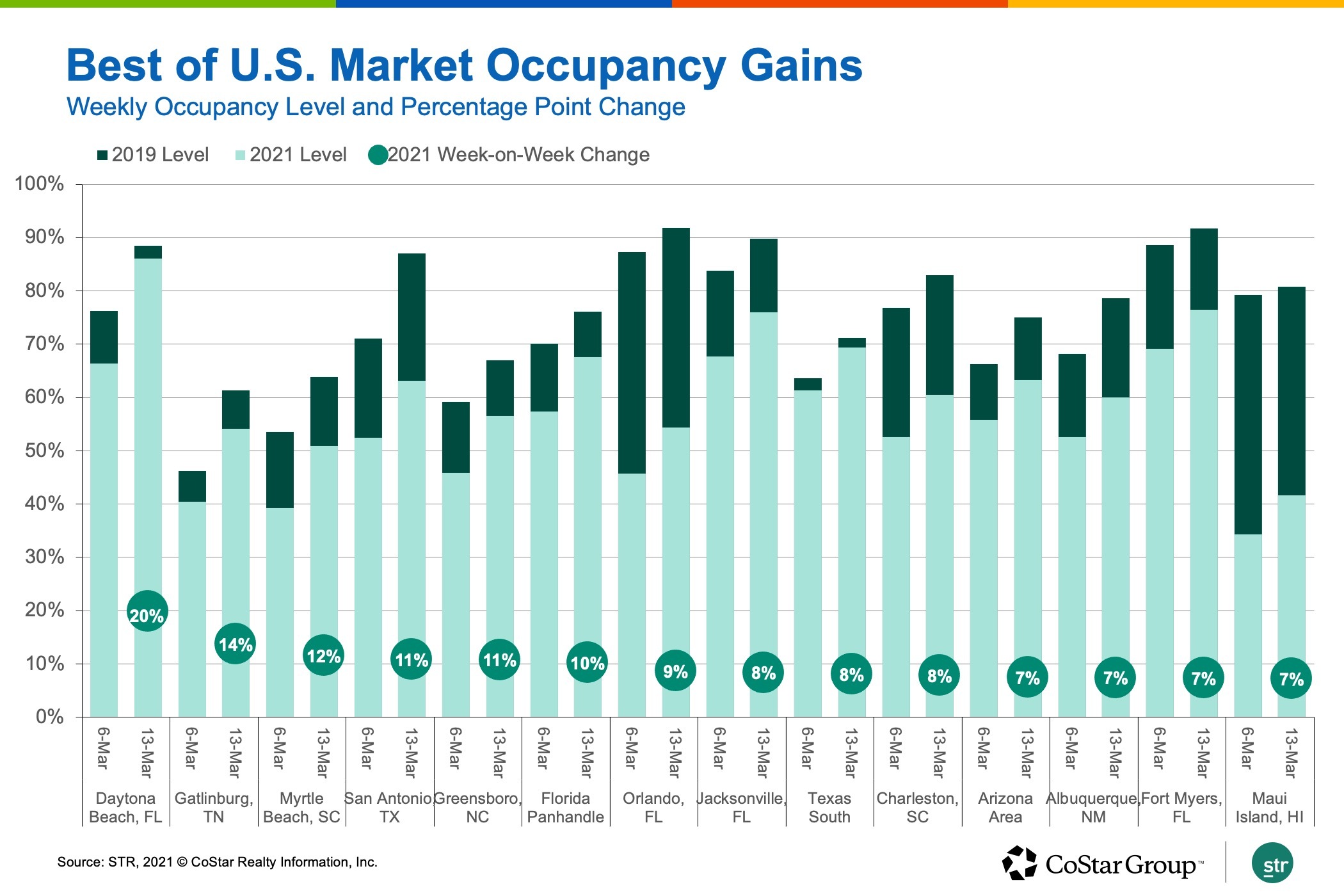

The rise in demand in Florida’s hotel market, as well as weekly occupancy, was the highest in the U.S., and demand for Texas hotels rose for the fourth consecutive week.

Along with Florida, hotel markets in Arizona, Texas, Alabama and Mississippi all posted occupancy above 60% for the week.

All Florida markets posted growth in hotel occupancy — led by the Florida Keys, which achieved the highest hotel occupancy in the U.S., as it has for the past eight weeks. Nine of the top 10 U.S. markets for weekly occupancy were in Florida.

Overall, nearly one quarter of all U.S. markets reported occupancy above 60% for the week, with peak performance on the weekend.

Still, total U.S. weekly occupancy remained about 25% lower than it was in 2019, though that percentage has improved in four of the past five weeks.

Weekly U.S. hotel average daily rate increased 4.2% over the prior week, marking the largest gain of the past four weeks. This performance was led by hotels outside of the U.S. top 25 markets.

All but 23 U.S. markets reported weekly ADR growth, led by Daytona Beach and other Spring Break destinations in Florida and elsewhere.

U.S. hotel ADR for the week was 76% of 2019 levels. Twelve markets — including the Florida Keys, Gatlinburg/Pigeon Forge and Daytona Beach — reported ADR that was above 2019 levels.

Isaac Collazo is VP Analytics at STR.

This article represents an interpretation of data collected by CoStar’s hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.